How workers’ compensation is evolving for the modern workforce

Prevention to protection

Table of Contents

I. Evolution and challenges of workers’ compensation in the U.S.

Since the enactment of Wisconsin’s landmark workers’ compensation law in 1911, the program has become a cornerstone of the American workplace, ensuring employees receive protection from crippling medical costs and lost income resulting from work-related injuries or illnesses.

By the late 1980s and early 1990s, the workers’ compensation system faced a period of instability. Spiraling medical costs and increasing lost-time expenses pushed combined ratios above 120%, raising concerns about the affordability and sustainability of coverage. Analysts cautioned that without intervention, the system could face collapse.

In response, nationwide reforms were enacted to restore financial balance and secure the future of workers’ compensation. These included measures to improve rate adequacy, contain medical costs, and align benefits with the evolving business environment. Corrective actions successfully resolved the immediate crisis and placed the system on a path to long-term health.

II. Current worker's compensation landscape

Recent data from the 2025 State of the Line report by the National Council on Compensation Insurance (NCCI) highlights the system’s robust performance1:

- The calendar year 2024 combined ratio stands at 86%, indicating strong financial health

- Industry-wide reserve positions total $16 billion, further underscoring stability.

- Lost-time claim frequency – cases resulting in disability income replacement – declined by 5% in 2024.

While these results reflect a decade of consistent strength, the workers’ compensation system continues to face evolving challenges. Economic factors such as worker shortages and wage inflation may drive up the severity of lost-time indemnity claims. Additionally, potential changes in the U.S. healthcare landscape could accelerate medical cost inflation, and new legislative or regulatory developments may threaten recent gains. As stakeholders look ahead, ongoing vigilance and adaptability will be essential to maintaining a strong and resilient workers’ compensation system that meets the needs of both employers and employees.

III. Influential factors in workers’ compensation claims

Fraud

Fraud committed against the workers’ compensation system is not a new trend. Receiving undeserved benefits by individuals, aided and abetted by networks of corrupt providers billing for unnecessary and costly diagnostic services, treatments and medical equipment, has been a staple of evildoers targeting the workers’ compensation system since inception. According to one report released in 2025, sophisticated fraud schemes cost the American workers’ compensation system between $35-$44 billion annually.11 In one case reported in October 2024, an Orange County, CA, man was charged for a third time in a fraud conspiracy with a local neurosurgeon and two others in a scheme that netted an estimated $100 million.12

An emerging fraud concern is the potential for criminals to deploy advanced artificial intelligence (AI) technologies that could make carrying out fraud even more profitable. Identity theft is also increasing in fraud committed in the automobile and construction sectors, where individuals have been caught trying to use false identification to secure employment as a fake employee “plant” to file fraudulent claims.

A growing overlap between medical providers and legal actors implicated in both auto and workers’ compensation fraud is illustrated by recent New York RICO action brought by ride-sharing giant Uber Technologies Inc. The lawsuit claims a group of law firms, doctors and pain-management clinics staged fake car accidents and performed unnecessary surgeries to take advantage of New York’s lucrative no-fault insurance policies.13

But AI and machine learning may place a new weapon in the anti-fraud arsenals of claims professionals, enabling the processing of vast amounts of claims data to identify patterns and anomalies. By leveraging predictive modeling, insurers can detect potential fraud even before it occurs rather than relying on traditional red flags visible only after the fact. AI-powered systems will enhance the process of claims triage by assigning risk scores to cases, helping insurers allocate investigative resources more effectively. Utilizing AI tools for routine tasks will also reduce human error and enable insurers to focus on high-risk claims while streamlining legitimate ones, strengthening fraud detection, reducing financial losses and improving customer experience.14

Climate change

Climate change, accepted as the engine driving the frequency and severity of extreme weather events, has shown to be increasingly responsible for unprecedented, dangerous heatwaves. Data indicates that more frequent high temperatures associated with climate change are the likely impetus for more heat-related injuries, or HRIs. A December 2024 report by the Workers’ Compensation Research Institute (WCRI) noted that HRIs, such as heat exhaustion and heatstroke, increased seven-fold on days when the temperature exceeded 90°F, versus days when temperatures range between 75°F to 80°F. In addition to a higher percentage of HRIs, the data suggests that higher temperatures contribute to greater frequency of other incidents, such as falls and cuts.2 This is, of course, especially concerning for construction projects, which typically require a significant percentage of outdoor work, exposing employees to stronger, longer-lasting heatwaves.

Concern over HRIs affecting workers has motivated a number of states to enact legislation regarding workplace heat stress. California's Heat Illness Prevention Standard requires employers to take action when the heat index – the combination of temperature and humidity – reaches 80°F, triggering requirements for shade, hydration and other ameliorative steps. Colorado, Minnesota, Oregon and Washington have also adopted state workplace heat-stress regulations affecting both external and internal environmental conditions.3 Workplace heat safety legislation was introduced for consideration in the Pennsylvania House of Representatives in August 2025. The bill requires employers to establish heat illness prevention plans, as well as providing workers with paid rest breaks, water and access to shade once the ambient heat index hits 80°F.4

Stress and mental health

A growing focus on mental health and well being both at and away from the workplace is also likely to impact the workers’ compensation system, as some states take steps to expand compensability with regard to trauma and Posttraumatic Stress Disorder (PTSD). During 2024, NCCI tracked 64 different state bills related to mental health compensability under workers’ compensation programs.5

Worker shortages

Worker shortages will be an ongoing concern, as changing economic and political conditions challenge the efforts of businesses in construction, manufacturing and service segments to recruit and retain the workers they need. As competition for workers increases, businesses may see accident and indemnity claims rise because new, younger hires are statistically more prone to accidents, with 35% of occupational injuries generated during their first year on the job.6 In 2021 and 2022, nearly 278,000 employees experienced an incident that resulted in days away from work – in their first 90 days on the job.7 At the other end of the age continuum, while aging workers are involved in just 13% of work-related injuries, those injuries are often more severe and require longer recovery times, with commensurate impacts on lost-time claims. By one measure, workers 75 years old and older are the fastest-growing group in the workforce, a percentage that has quadrupled since 1964. When injured, members of this age cohort may drive higher medical bills and recover more slowly, resulting in greater disability claims.8

Medical cost inflation

Rapidly rising medical cost inflation will continue to challenge workers’ compensation programs. According to the NCCI’s 2025 State of the Market report, while overall claims dropped 5%, both medical and indemnity costs rose 6% in 2024. Indications are that the rise in medical costs was primarily due to increases in utilization, with injured workers seeing doctors and being evaluated more often as costs increasing in every medical category, from office visits to inpatient and outpatient surgery.9

Opioid abuse

Costs associated with opioid abuse continue to impact workers’ compensation claims. Historically, the overprescription and abuse of addictive opioids has had profound implications for the health of workers, placing additional stress on employees, employers and the workers' compensation system by complicating recoveries and lost worktime. A 2017 report from the Workers' Compensation Research Institute (WCRI) reported 44% of workers' compensation claims included at least one prescription for opioids. While the WCRI report predated COVID-19, indications are that opioid misuse and overdose increased during the pandemic as many were isolated from traditional support systems.10

IV. Workers’ compensation issues by industry

Below is a view of workers’ compensation trends, challenges and potential solutions for business segments employing significant cross-sections of American workers:

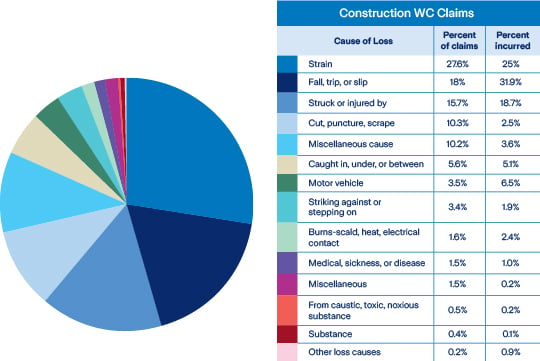

Construction

While technology advances have helped make jobsites much safer, construction remains inherently riskier than other business segments. The potential for serious injuries and lost-time claims associated with heavy equipment, falls and other accidents remains higher than other workplaces. Claims data from Zurich’s RiskIntelligence platform confirms the three primary causes of jobsite injuries – strains, slips, trips and falls, and “struck by” – account for 60% of total workers’ compensation claims and 75% of incurred losses, with very little change year- on-year.22

But heightened concern regarding the mental health and well-being of construction workers is trending upward within the industry. There is some evidence that construction workers’ compensation claims for mental stress are on the rise, suggesting that awareness is gaining traction. While the number of construction industry mental stress claims reported by Zurich is dwarfed by the typical causes of workplace injuries and disabilities, claims for mental stress have increased approximately 32% year- on-year.

Statistically, construction workers are known to have higher suicide rates than workers in other fields. By one estimate, about 5,000 construction workers die by suicide annually.15 Additionally, the construction industry continues to see high rates of drug use, contributing to the highest overdose deaths by occupation, according to the Centers for Disease Control and Prevention (CDC). Nearly half of construction workers report symptoms of anxiety and depression, but fewer than 5% seek professional help, compared to 22% of the general U.S. population.16

The combination of high-hazard work environments, long hours, family separations due to often far-flung jobsites, and the job insecurity that often goes with the territory for construction workers makes them particularly vulnerable. According to the Associated General Contractors of America (AGC), breaking the stigma about seeking help for mental

health issues, encouraging workers dealing with stress and trauma to seek help, and training supervisors to more effectively recognize when intervention may be needed should all be part of normalizing conversations about mental health in the construction industry.17

Comprehensive workplace policies are essential in addressing one of the key indicators of stress, trauma and pain management issues among construction workers – the aforementioned crisis of opioid abuse. Drug-free workplace protocols, employee assistance programs, and peer support networks can be vital in prevention and recovery. Education for both employees and employers on the risks of opioids as well as alternative pain management approaches can help to address any problems that may exist in a given workplace and help mitigate impacts on workers’ compensation programs.18

One construction industry trend showing no signs of slowing is the goal of reducing workplace injuries and illnesses through increasing investments in innovative worker safety technologies by employers. While some of the following are already in wide use, or should be, innovations in the technology development pipeline will continue to help reduce the risks of the modern construction jobsite:19

- Wearables – Smart helmets, vests and glasses equipped with sensors and communication devices help monitor the vital signs of workers and detect hazardous conditions, providing real-time information to wearers and supervisors.

- Drones – Drones enhance safety in a variety of roles, such as providing aerial surveys, monitoring work progress and assessing a site from a bird’s eye view. Drones can also inspect hard-to-reach areas that might otherwise place a worker at risk.

- Internet of Things (IoT) – Connectivity through the IoT can allow individual pieces of equipment to function as parts of a collaborative whole. IoT-enabled sensors can also monitor the condition of machinery, the structural integrity of the project at various stages, and even track environmental conditions.

- Building Information Modeling (BIM) – BIM technology enables the creation of realistic, digital 3D models of a project, providing comprehensive views of the entire construction process, allowing better planning to reduce dangerous situations.

- Autonomous & remote-controlled machinery – Similar to benefits of drones, autonomous and remote-controlled construction machinery can handle tasks in high-risk situations.

- Augmented reality & virtual reality – AR and VR technologies can provide training and simulate dangerous scenarios, providing workers with virtual safety training before stepping into the project

Manufacturing

The integration of advanced robotics and AI-enhanced automation is reshaping the manufacturing industry across the entire spectrum of industrial and consumer products. As in the construction field, robots are being called upon to perform in an expanding range of high-risk, repetitive and dangerous tasks with the potential to place human workers at risk.20

But while robots are freeing workers from potentially hazardous tasks, manufacturers need to ensure that they understand any new risks that may arise when humans are working alongside robots on production lines or on the factory or warehouse floor. Have steps been taken to ensure that robots are “smart” enough to avoid injuries to humans if they get in the way? Have workers received the appropriate training to ensure their personal safety when working with or around robots?

Another trend impacting manufacturing is the integration of AI-powered predictive maintenance of production equipment. It is not uncommon for key pieces of equipment to fail at the worst possible times, potentially causing injuries to employees operating the equipment. AI-enabled monitoring of production equipment can predict failures before they occur, helping to avoid a catastrophic event.

As in construction, another innovation gaining adherents in manufacturing is the application of virtual reality (VR) and augmented reality (AR) technologies that allow employees to engage in realistic workplace scenarios without physical risks, simulating hands-on learning for operating complex machinery and emergency procedures.21

Finance, private equity & professional services

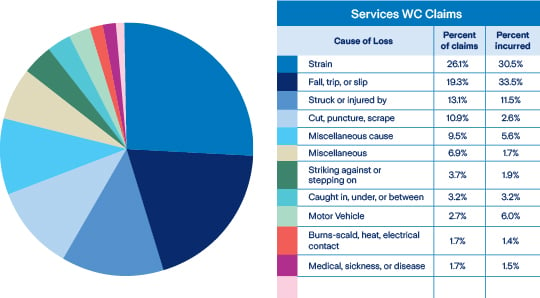

Generally considered “low risk,” but not risk free, financial services, private equity and other professional services, categorized as “Combined Office” by NCCI, share most of the same workers’ compensation risks. From slips, trips and falls to repetitive stress, eye strain, manual handling (such as moving a box of office materials from storeroom to desk) and ergonomic claims due to poorly designed workspaces, there are few significant risk differences associated with these organizations. According to claims data from Zurich’s RiskIntelligence platform, workplace incidents associated with strains, slips, trips and falls, and “struck by” in service related industries generate results roughly similar to those of construction – around 58% of claims and 75% of incurred losses.22

Like other business segments, these classes face evolving workers’ compensation risks such as the compensability of work-related mental health claims, the impacts of substance abuse on claim duration, and rising medical claim inflation.

Workers’ compensation programs for office exposures also face the challenge of effectively monitoring ergonomic issues (posture, workspace design, etc.) not only in the office but for home workers as well. Because many of the business segments falling within NCCI’s combined office class are highly “remote-friendly,” increased ergonomics related claims can result from postural habits carrying over from poorly designed home workspaces, impairing readjustment to normal workplace design upon returns to office settings, whether periodic or long-term.

V. Looking ahead

According to the NCCI and other industry observers, the outlook for the health and security of the workers’ compensation system is very positive. Predictions are that the line will continue to be a stable, financially secure and competitive market for the foreseeable future. Because market conditions can change relative to any line of coverage, insurers and customers need to stay abreast of trends in workers’ compensation, and take steps that can help them reduce costs even during the current, favorable market environment, including:

- Monitor developing regulatory actions related to workplace safety proposed in every state where the business may have employees. Specific regulations can and do vary from state to state.

- Continue to allocate resources to investigate, acquire and implement enhanced workplace safety technologies available to help prevent workplace accidents.

- Make sure the organization has a range of return-to-work alternatives designed to respond to variations in the restrictions recovering employees may face based on the nature of their injuries.

- Train and continuously update supervisors and managers about emerging workplace regulations and workers’ compensation trends.

- Conduct annual reviews of the workers’ compensation program to ensure that it is meeting the organization’s changing requirements and evolving regulations.

Most importantly, immediately report and thoroughly document any workplace incident to the insurance carrier or state program, even if immediate emergency medical intervention was not required. A fall, sprain or strain while lifting a heavy object could result in a potential claim at a later date. And delays in reporting can complicate a claim by making it more difficult to verify all the facts of a case as well as potentially opening the door to fraud.

VI. The value of data

For companies, accessing the insights embedded in claims data in collaboration with their insurance carriers can be a gold mine for identifying ways to better control and potentially reduce costs. Data drives the workers’ compensation system, providing insights to improve workplace safety, enhance claim outcomes, and support the organization’s risk management objectives. All of which is why choosing an insurance provider with a robust and reliable platform for the analysis and delivery of data about a customer’s workers’ compensation program is critical to the program’s success. One example is Zurich’s RiskIntelligence platform, which provides year-over- year performance insights, full reporting capabilities and benchmarking to peers within the same industry – data that has been shown to help drive more effective risk management strategies.

Even at a time when the workers’ compensation marketplace is historically strong and predictable, maintaining a clearer view of the factors driving claim trends can be a key step in reducing an organization’s overall cost of risk, making the workplace safer for employees and more productive and profitable for businesses.

References

- Glenn, Donna, FCAS, MAAA, Chief Actuary. “AIS 2025 Highlights Report – State of the Line Report.” National Council on Compensation Insurance (NCCI). 14 May 2025. https://www.ncci.com/Articles/Pages/Insights-AIS2025-SOTL.aspx

- Thumula, Vennela, Fomenko, Olesya. “Heat-Related Illnesses in the Workplace – A WCRI Flash Report.” 18 December 2024. https://www.wcrinet.org/reports/heat-related-illnesses-in-the-workplacea-wcri-flashreport

- "Heat.” Occupational Safety & Health Administration – U.S. Department of Labor. https://www.osha.gov/heat-exposure/standards

- “Pennsylvania could be the next state with a worker heat rule. Safety+Health. 12 September 2025. https://www. safetyandhealthmagazine.com/articles/27291-pennsylvania-could-be-the-next-state-with-a-worker-heat-rule

- Araullo, Kenneth. “NCCI reports on workers' comp reforms and trends in 2024.” Insurance Business. 9 September 2024. https://www. insurancebusinessmag.com/us/news/workers-comp/ncci-reports-on-workers-comp-reforms-and-trends-in-2024-504799.aspx

- "New workers account for 35% of injuries, analysis of comp claims shows.” Safety+Health. 13 July 2022. https://www. safetyandhealthmagazine.com/articles/22780-new-workers-account-for-35-of-injuries-analysis-of-comp-claims-shows

- "Safety at work: The first 90 days.” Safety+Health. 23 March 2025. https://www.safetyandhealthmagazine.com/articles/26567 safety-at-work-the-first-90-days

- “20 Workers Comp Issues To Watch in 2025.” International Risk Management Institute (IRMI). 14 February 2025. https://www.irmi.com/articles/expert-commentary/20-workers-comp-issues-to-watch-in-2025

- Esola, Louise. “Workers compensation line remains successful despite rising costs: NCCI.” Business Insurance. 13 May 2025. https://www.businessinsurance.com/workers-compensation-line-remains-successful-despite-rising-costs-ncci/

- Muselman, Claire. “The Ongoing Opioid Crisis: Impacts on the Workers’ Compensation Industry.” WorkersCompensation.com.” 14 July 2024. https://www.workerscompensation.com/daily-headlines/the-ongoing-opioid-crisis-impacts-on-the-workers compensation-industry/

- Recamara, Josh. "Revealed – Workers’ comp fraud costs up to $44 billion each year." Insurance Business. 27 March 2025. https://www.insurancebusinessmag.com/us/news/workers-comp/revealed--workers-comp-fraud-costs-up-to-44-billion-each year-530050.aspx

- Araullo, Kenneth. “Man charged in $100 million workers’ comp fraud scheme” Insurance Business. 18 October 2024. https://www.insurancebusinessmag.com/us/news/legal-insights/man-charged-in-100-million-workers-comp-fraud scheme-510365.aspx

- Nahmias, Laura, Lung, Natalie. “Uber Alleges Fraud Scheme by New York Groups Faking Car-Crash Injuries.” Insurance Journal. 31 January 2025. https://www.insurancejournal.com/news/east/2025/01/31/810277.htm

- Recamara, Josh. "Revealed – Workers’ comp fraud costs up to $44 billion each year." Insurance Business. 27 March 2025. https://www.insurancebusinessmag.com/us/news/workers-comp/revealed--workers-comp-fraud-costs-up-to-44-billion-each year-530050.aspx

- Raffetto, Caroline. “Construction’s Mental Health Crisis: Suicide Rates and Solutions” Springfield State Journal-Register. Construction Owners Club. 20 January 2025. https://www.constructionowners.com/news/constructions-mental-health-crisis suicide-rates-and-solutions

- Ibid.

- Ibid.

- Muselman, Claire. “The Ongoing Opioid Crisis: Impacts on the Workers’ Compensation Industry.” WorkersCompensation.com.” 14 July 2024. https://www.workerscompensation.com/daily-headlines/the-ongoing-opioid-crisis-impacts-on-the-workers compensation-industry/

- “New Safety Technology in Construction to Reduce Incidents.” American Institute of Constructors. 15 January 2024. https://aic-builds.org/new-safety-technology-in-construction-to-reduce-incidents/

- Rafi, MD. "What the Future of Workplace Safety Looks Like." Manufacturing.net. 25 May 2025. https://aic-builds.org/new-safety technology-in-construction-to-reduce-incidents/

- Ibid.

- Zurich RiskIntelligence, WC claims data, 23 September 2025

The information in this publication was compiled from sources believed to be reliable for informational purposes only. All sample policies and procedures herein should serve as a guideline, which you can use to create your own policies and procedures. We trust that you will customize these samples to reflect your own operations and believe that these samples may serve as a helpful platform for this endeavor. Any and all information contained herein is not intended to constitute advice (particularly not legal advice). Accordingly, persons requiring advice should consult independent advisors when developing programs and policies. We do not guarantee the accuracy of this information or any results and further assume no liability in connection with this publication and sample policies and procedures, including any information, methods or safety suggestions contained herein. We undertake no obligation to publicly update or revise any of this information, whether to reflect new information, future developments, events or circumstances or otherwise. Moreover, Zurich reminds you that this cannot be assumed to contain every acceptable safety and compliance procedure or that additional procedures might not be appropriate under the circumstances. The subject matter of this publication is not tied to any specific insurance product nor will adopting these policies and procedures ensure coverage under any insurance policy. Insurance coverages underwritten by individual member companies of Zurich in North America, including Zurich American Insurance Company. Certain coverages not available in all states. Some coverages may be written on a nonadmitted basis through licensed surplus lines brokers. Risk engineering services are provided by The Zurich Services Corporation.