Critical Illness Insurance

A Strategic Approach to Employee Well-being

Supporting employee well-being is more than a benefit—it’s a strategic priority. Critical Illness Insurance helps your workforce prepare for unexpected health challenges, such as cancer, heart attacks, or strokes. This coverage provides a lump-sum benefit, as defined in the policy, that can be used to help address eligible expenses following a covered diagnosis.

By offering Critical Illness Insurance, your business demonstrates a commitment to health and security, reinforcing your organization’s broader workforce strategy. It complements existing benefits, creating a more complete approach to well-being that aligns with your organization’s values and goals.

Incorporating Critical Illness Insurance into your benefits strategy supports broader workforce governance objectives.

Why choose Zurich for critical illness insurance

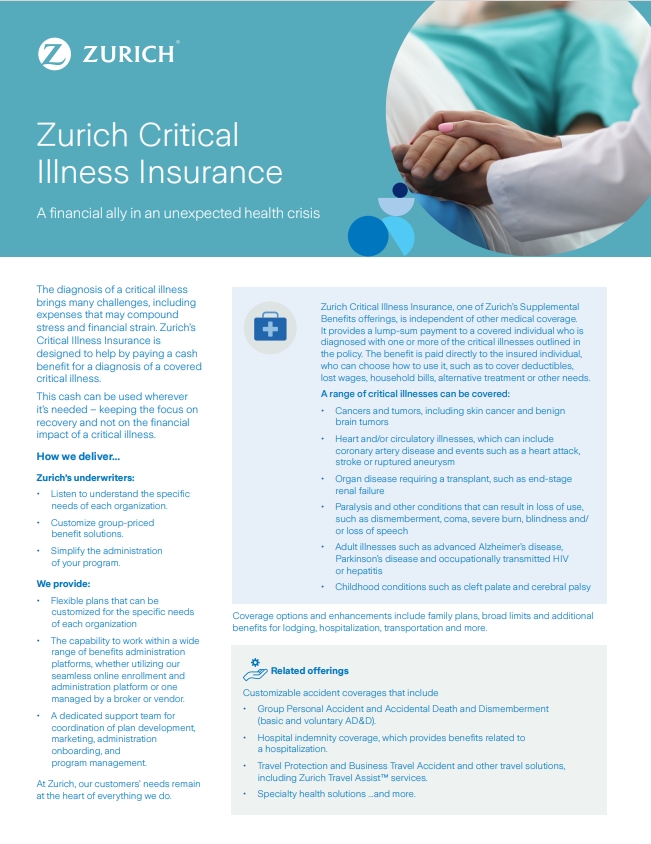

The strength of Zurich’s Critical Illness Insurance goes far beyond policy details. We offer a dedicated support team for coordination of plan development, marketing, administration onboarding, and program management. We provide you with a single point of contact, as well as administration that details processes, forms, and group/individual contact information. We’ll work with you to help simplify the administration of your program and we’re always ready to answer questions to help address your needs and those of your members or employees.

At Zurich, our customers’ needs remain at the heart of everything we do.

Related insurance offering

Examples of critical illnesses covered

Critical Illness Insurance provides a lump-sum benefit upon diagnosis of a covered condition. For an employee who experiences a heart attack, the benefit can help cover out-of-pocket medical expenses, lost income, or even household bills. Similarly, if an employee is diagnosed with cancer, the funds can support treatment costs or other unexpected expenses.

This coverage is designed to provide financial flexibility during challenging times, in accordance with policy terms. It’s important to review policy documents for specific details, as coverage may vary.

Critical Illness Insurance is not a replacement for health insurance but a valuable supplement to help manage the costs of life-altering conditions.

Critical illness coverage options and enhancements include family plans, broad limits and additional benefits for lodging, hospitalization, transportation and more. A range of critical illnesses can be covered, including:

Want to learn more?

Connect with our Customer Inquiry Center for more information.

FAQs

Offering Critical Illness Insurance to your employees or group members can be a valuable part of a benefits package. For employers, a critical illness option shows current employees and potential new hires that you are concerned for their well-being and financial stability, helping you attract and retain top talent. For affinity groups, offering the coverage can be a real competitive edge in reaching new customers and members.

Zurich’s flexible plans can be customized for the specific needs of each organization and within a wide range of benefits administration platforms. We have a dedicated support team for coordination of plan development, marketing, administration onboarding, and program management.

Critical Illness Insurance enhances traditional health coverage by providing a lump-sum payment directly to the insured upon diagnosis of a covered condition. While health insurance covers medical expenses like treatments and hospital stays, this benefit offers financial flexibility to address out-of-pocket costs, household bills, or other financial obligations.

By supplementing traditional health insurance, this coverage addresses additional financial considerations following a covered diagnosis. For businesses, offering it demonstrates a commitment to employee well-being and supports workforce risk planning efforts.

Incorporating Critical Illness Insurance into your benefits package is a proactive way to address financial vulnerabilities, helping employees manage unexpected costs and reinforcing the resilience of your benefits program.

1. Rosenthal, Meredith B. “The Growing Problem of Out-of-Pocket Costs and Affordability in Employer-Sponsored Insurance.” JAMA (Journal of the American Medical Association), Vol. 326, No. 4. 27 July 2021.